Event-Driven Investments: Get the Alpha, Forget the Beta

Key Takeaways

1. Event-driven investment strategies are capable of generating good income streams, while being less correlated to the general market.

2. Event-driven strategies are typically short-term investments, and capital allocated to such strategies can be redeployed quickly to other areas in response to changing market conditions. This flexibility makes them a good choice for P&C investment portfolios.

The Need to Increase Investment Income

A sizable portion of P&C companies’ insurance portfolios comprises of high-grade bonds. In the past, when interest rates were higher, these bonds also provided them with satisfactory income. Over the past decade, however, as interest rates have declined, interest income has declined as well.

It is likely that the low-interest rate environment will continue for some time yet. On June 10, 2020, the US Federal Reserve (Fed) announced that it plans to keep short-term interest rates at the current near-zero level through 2022. This does not spell good news for the investment portfolios of bond-heavy P&C insurance companies.

We have written about the low rate environment and how they influence P&C investment policies. Here we focus on a narrower problem: are there ways by which a P&C company can offset the loss of interest income without taking on too much risk? The answer, as we shall show below, is yes, and it applies to any general interest rate environment.

How Event-Driven Investing Can Lower Risk and Improve Returns

Insurance companies take care to write business so that client claims are uncorrelated or independent of each other. The same principle suggests that having uncorrelated asset classes in their investment portfolios can help lower investment risk.

Examples of assets that have less correlation with equity markets are gold, real estate, commodities, currencies, and event-driven portfolios.

At Alpharay Insurance, we favor event-driven investing. Examples of event driven investing range from conventional strategies such as “merger-arbitrage” and participation in tender offers, to unconventional strategies such as investing in legal claims or investing in electricity congestion markets.

Many of these event-driven opportunities are short-term in nature; in fact, some investments from start to finish take only a few weeks. When such event-driven opportunities present themselves, one needs to: a) determine the length of time of the required capital commitment, b) calculate or quantify the potential gains, and, c) assess the probability of a favorable outcome. Besides quantitative factors, sound qualitative judgement is also needed before deciding to commit capital to such investments. Since the outcomes from event-driven investments are inherently uncertain, there will be some instances when the investments will lose money, even with careful analysis. Nevertheless, from our past experience, they have an expected value of generating 3%-5% returns per opportunity, averaged over both winners and losers.

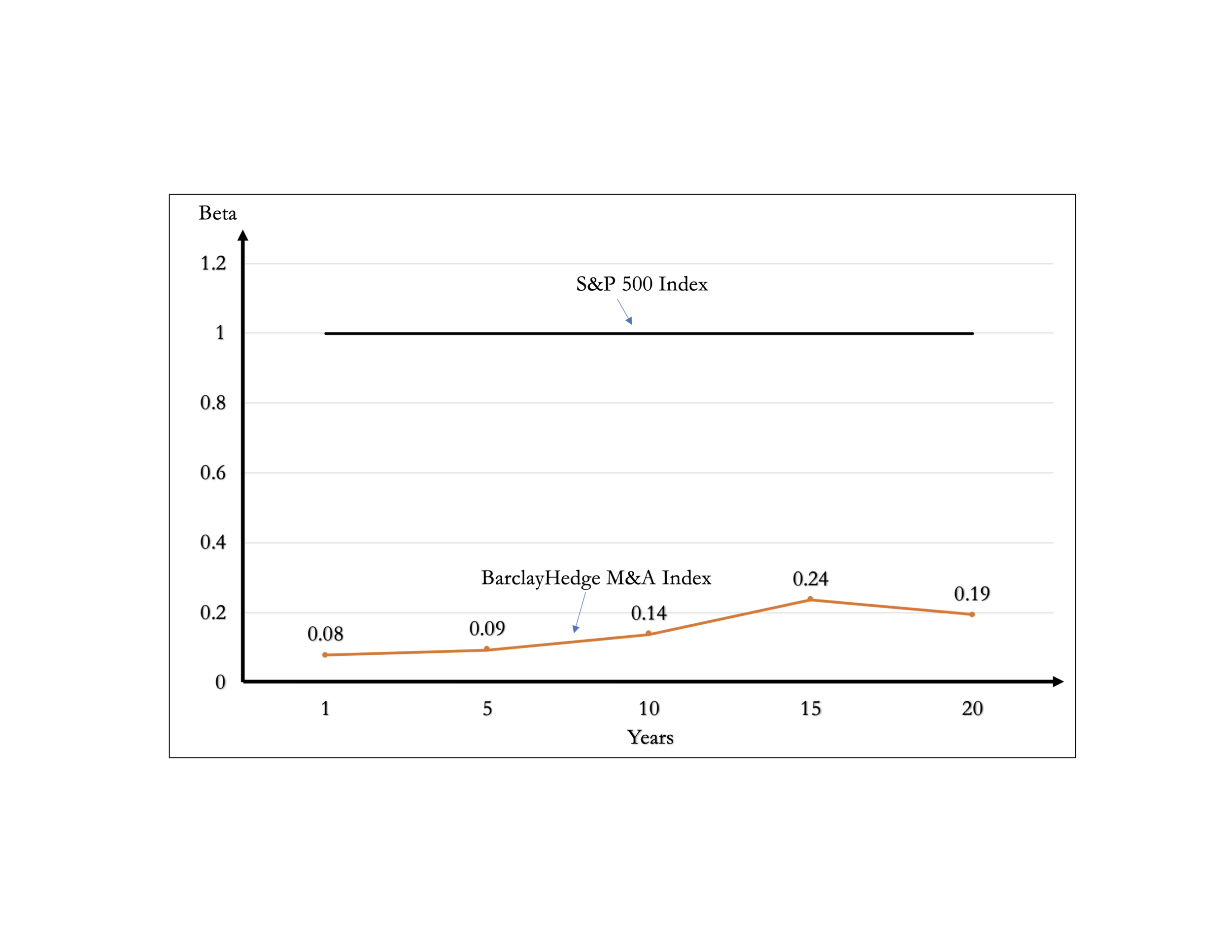

One advantage of many event-driven opportunities is that they are mostly uncorrelated to daily market movements. In industry jargon, they have a beta lower than 1. An investment that has a beta of 1 implies that it is exactly correlated with the market. Lower the beta, less the correlation with the general market.

In the figure below, the orange line shows the beta of BarclayHedge M&A index as calculated over different time-horizons; as reference, the beta of the S&P 500 Index is represented by the black line. The beta of the BarclayHedge M&A index is clearly very low across all time horizons.

Source: Historical data are from www.BarclayHedge.com and www.Multpl.com. Numbers are calculated based on monthly returns.

In calculating its Best Capital Adequacy Rating (BCAR), A.M Best assesses a high capital charge for stocks but adjusts for the beta of the investment portfolio. Thus, low beta investments will get a favorable treatment in BCAR calculations.

Another advantage of event-driven investments is that since they are short-term in nature, capital is not tied up for too long in any investment and therefore can be quickly redeployed to other promising opportunities should the need arise. This flexibility gives such event-driven investments high option value.

W. R. Berkley, a stockholder-owned P&C company, has been an enthusiastic participant in merger arbitrage and related activities for many years. In 2019, for example, it committed nearly $450M in capital (out of shareholder’s equity of $6.1B) to merger arbitrage activities and earned $34.5M in pre-tax for a very impressive return of 7.8%. This was not a fluke result. For example, in 2018, W. R. Berkley earned a pre-tax return of 4.7% on nearly $600M of capital committed to merger arbitrage activities.

Another example is that of Warren Buffett’s Berkshire Hathaway. Before it became a behemoth that it is today, it took active part in merger-arbitrage activities. Warren Buffett has written several times in his shareholder reports about the outsized gains that he was able to generate from such activities.

In our experience, event-driven investing opportunities are plentiful and offer fertile ground for earning decent investment returns. P&C company executives would be remiss if they did not seriously consider event-driven investing to be part of their investing toolkit.

How a P&C Company can participate in Event-Driven Investing

An insurance industry Chief Investment Officer (CIO) wanting to invest in event-driven opportunities has a couple of choices. The CIO can take a page from W. R. Berkley and set up a specialized in-house segment that is dedicated to such investing opportunities. This would require a significant commitment of resources.

Alternatively, the CIO can outsource such investments to a specialist firm such as Alpharay Insurance Services, which will allow the insurance company to focus on its core areas.

Either way, event-driven investing offers rich opportunities for P&C companies to pursue alpha without the beta.

Sources: Company filings