A Capital Method for Managing P&C Investment Portfolios

Key Takeaways

1. Managing P&C investment portfolios is very different than managing other investment funds. Proper management of the P&C investment portfolio is possible only if capital in the overall P&C balance sheet is allocated correctly across all its lines of business.

2. Two critical factors in determining the right asset mix in a P&C company’s portfolio are its desired financial rating and its opportunity cost of capital of non-portfolio management activities. The right asset mix varies by P&C company.

Managing P&C Investment Portfolios is Different than Managing Other Investments

Choosing an investment policy for a P&C company is very different than choosing it for an investment fund or a hedge fund. For example, consider a hedge fund that has an asset allocation of 80% to bonds and 20% to stocks. If market conditions change dramatically and the hedge fund manager thinks that stocks are a more attractive investment, the manager can in short order change the asset allocation to 100% stocks. A Chief Investment Officer (CIO) of a P&C company may be in complete agreement with the hedge fund manager as to the relative attractiveness of stocks, but the CIO would find it almost impossible to achieve the same reallocation in the P&C investment portfolio. This is because, as we shall see below, the composition of the P&C investment portfolio also affects other elements on the company’s balance sheet.

P&C Investment Portfolio Composition Affects Capital Required

A P&C company’s raison d’être is to meet its obligations to its policy holders, and its ability to do so is measured by its financial rating. A widely used metric, called Best’s Capital Adequacy Rating or BCAR, estimates a P&C company’s financial strength by estimating the risk of its investments and the risk of its reserves and calculating whether it has sufficient capital to meet policy holder obligations under various risk scenarios.

The composition of the investment portfolio affects the calculation of financial strength. Government bonds are considered riskless, corporate and municipal bonds are assumed to be slightly risky, and stocks are considered to be even riskier. Without getting into the intricacies of BCAR calculations, it is possible to say that the riskier the asset class in the portfolio, the more the capital that has to be held if the financial strength of a P&C company is to stay unchanged.

Determining the Right Asset Mix in the P&C Investment Portfolio

State Farm Group, a mutual company, is the largest P&C insurance company in the US. Common and preferred stocks comprise a whopping 50% of its investing assets. Travelers Group is a large stockholder-owned P&C insurance company. Stocks only comprise 0.5% of its investments, with pristine bonds making up the bulk of its investments. Both these companies are rated very highly on their financial strength. State Farm gets the highest A++ rating from A.M. Best, while Travelers gets an A+ rating.

Figure 1. Investment asset mix for State Farm and Travelers

Two good companies with wildly different stock allocations! Do either or both of them have the correct asset mix? If not, can the asset mix be improved? How should the right asset mix look like?

To investigate these questions, we give a simplified exposition for how a P&C company should choose the best asset mix in its investment portfolio. Consider two asset classes, stocks and high-quality bonds, and assume that the financial rating should remain the same regardless of the asset mix.

If bonds are better value than stocks, the correct portfolio allocation rule is to simply put 100% of its investments in high-quality bonds. Since high quality bonds require very little capital, most of the capital can be allocated to non-portfolio business lines.

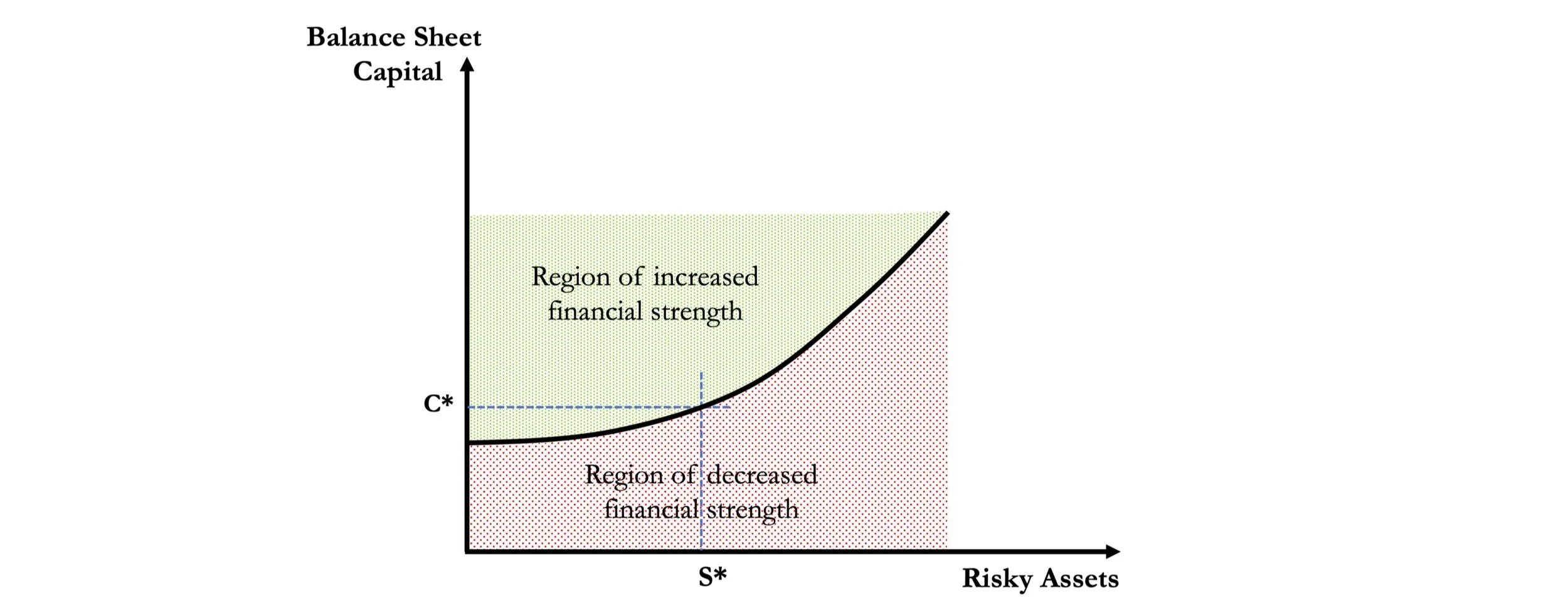

If stocks are better value than bonds, then things get interesting. If financial strength is to remain at desired levels, the company has to hold more capital on its balance sheet as the stock holdings in the portfolio increase. The figure below illustrates that the capital needs are relatively small at low levels of stock holdings but increase significantly at higher levels of stock holdings. This is because BCAR calculations penalize higher levels of stock holdings.

Figure 2. More capital is needed to support stock investments

Because of the increased capital requirements at higher levels of stock holdings, we can expect a diminishing return of the investment income per dollar of capital --- earned when an extra dollar of capital on the balance sheet is committed to increase stocks in the investment portfolio. This is represented by the black downward sloping curve in Figure 3. The green line in Figure 3 shows the P&C company’s opportunity cost of capital of non-portfolio management activities or simply opportunity cost of capital (to avoid saying a mouthful). The opportunity cost of capital is how much money the company will earn per dollar of capital invested on an alternative activity (other than portfolio management activities). Alternative uses of capital include writing new business, making acquisitions, stock buybacks (if it’s a stock P&C company), etc. In the figure below, the P&C company should continue committing capital to increase stock allocation in the portfolio until the capital committed reaches C*.

Figure 3. Efficient capital allocation

From Figure 2, the point C* corresponds to the stock holdings S*. This is the company’s optimal asset mix: allocate S* to stocks and the rest to bonds. One can interpret C* to be the capital held in the balance sheet to support the investment portfolio; similarly, the remaining capital can be interpreted as being allocated to other business lines so that the desired financial strength is maintained.

If the company were to allocate less than S* in stocks in its investment portfolio, then the company is leaving money on the table, as it will be committing capital less than C* to support its investment portfolio (corresponding to a point to the left of C* in Figure 3), where it is capable of earning more from the investment portfolio than from other opportunities.

If the company were to allocate more than S* in stocks in its investment portfolio, then the company is earning sub-par returns on its capital, as it will be committing more than C* to support its investment portfolio (corresponding to a point to the right of C* in Figure 3), where it is capable of earning more from non-portfolio management activities.

The analysis we presented here is a simplified one. An actual P&C company has a lot of moving parts, and the capital allocation process will need to simultaneously consider those factors as well. For example, allocating capital to increase insurance float will also result in increased investments, and those need to be optimized as well, subject to maintaining desired financial strength. But the core principle of capital allocation will be the same.

The bottom line is that the P&C company can efficiently allocate capital across all its business lines based on the higher of the investment income per dollar of capital or the company’s opportunity cost of capital. As a by-product, this will also determine the right asset mix for a P&C investment portfolio. The right asset mix depends on the company’s opportunity cost of capital and its desired financial strength.

The opportunity cost of capital varies by company. For example, we estimate that the opportunity cost of capital for State Farm is quite different than for Travelers today. Similarly, the financial strength also varies by company. Even if two companies were in complete agreement on the relative merits of one asset class versus another, the right asset mix for each company could be different if they had different opportunity costs of capital and different financial ratings. This leads to another, perhaps more surprising, conclusion.

The correct asset mix for each P&C company could be different: there is no one-size-fits-all investment policy applicable to all P&C companies.

How P&C Executives can Allocate Capital Efficiently and Manage their Investment Portfolio

Alpharay Insurance Services specializes in performing the analysis presented here. We do this by taking an in-depth look at various factors such as the opportunity cost of capital; the relative valuations of stocks, bonds, and other asset classes; the effect of potential market declines on financial rating; BCAR estimates under various risk scenarios; etc. Such analysis can be used by P&C company management to ensure that capital is allocated to its best use and to find the right asset mix in their portfolio.

Sources: Company filings